In 2008, an obscure cryptography message board received a post from user Satoshi Nakamoto. Titled Bitcoin: A Peer-to-Peer Electronic Cash System, this whitepaper introduced the world to Bitcoin, a completely digital currency that was built on a decentralized, peer-to-peer network and the genesis of the digital assets known as cryptocurrencies. Though electronic cash and payment systems had previously existed, such as PayPal, what made Bitcoin unique was the innovative combination of a distributed ledger system along with cryptographically secure information transmission; thanks to these two core characteristics, the Bitcoin protocol proved to be anonymous, private, and immutable. These features made Bitcoin popular with groups familiar with cryptography, the art of protecting and securing information. The data-security experts in the cryptography forums lauded Bitcoin for its ability to serve as a truly private, protected form of peer-to-peer transacting, completely removing the need for a third-party to act as a facilitator.

Bitcoin was capable of acting as a secure, peer-to-peer transaction platform thanks to the underlying software protocol. This protocol was a form of distributed ledger technology. Distributed ledgers are forms of data management where the record of data, such as a transaction history or log of values associated with given accounts, exists across several nodes as opposed to one central server or warehouse. This creates redundant, publicly verifiable records of transaction history, building stability and immutability into the system. Distributed systems are more resistant to outside attempts at interference, such as hacking, and malicious attempts to gain control of the system. Thanks in large part to the inherent security features of distributed systems, they were a natural choice as a foundation for the protocol underlying Bitcoin.

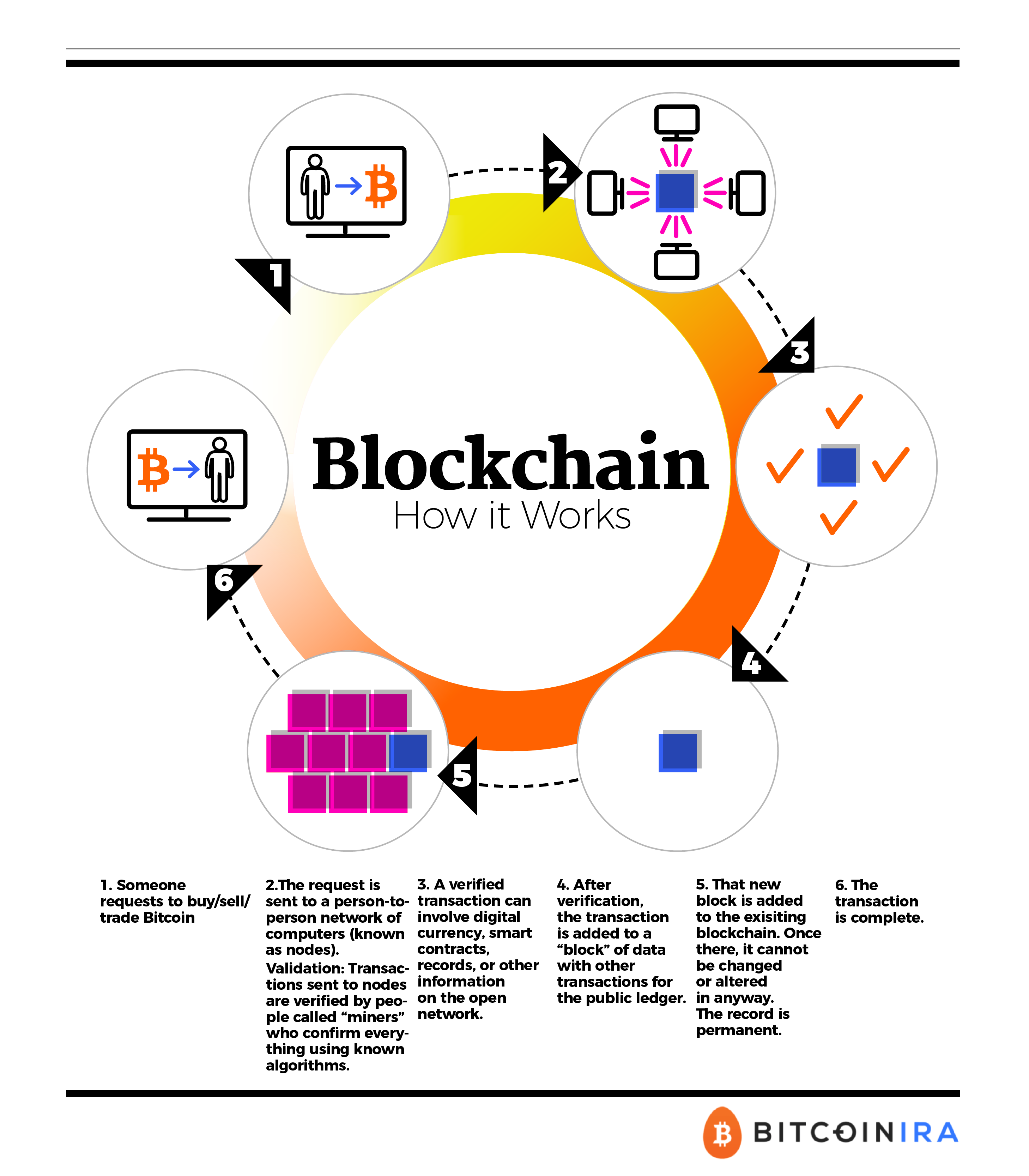

This protocol is called blockchain. Blockchain is a form of distributed ledger where new transactions and interactions added to the ledger are collected and verified in groups referred to as blocks. A block is a cluster of transactions, gathered and cryptographically proven. Every ten minutes, a block is verified across the public ledger, granting each user in the network the ability to view the entirety of the network’s transaction history. This history is made up of a long chain of blocks of transactions, thus the name ‘blockchain’.

3,500+ 5-Star Reviews

3,500+ 5-Star Reviews