Key Sections

The Internal Revenue Service (IRS) has introduced new reporting standards as digital asset activity continues to expand across financial markets. As cryptocurrencies and related transactions become more widely used, additional frameworks are being developed to support consistent reporting. Understanding Form 1099-DA provides context on how certain digital asset transactions may be reported under these evolving guidelines.

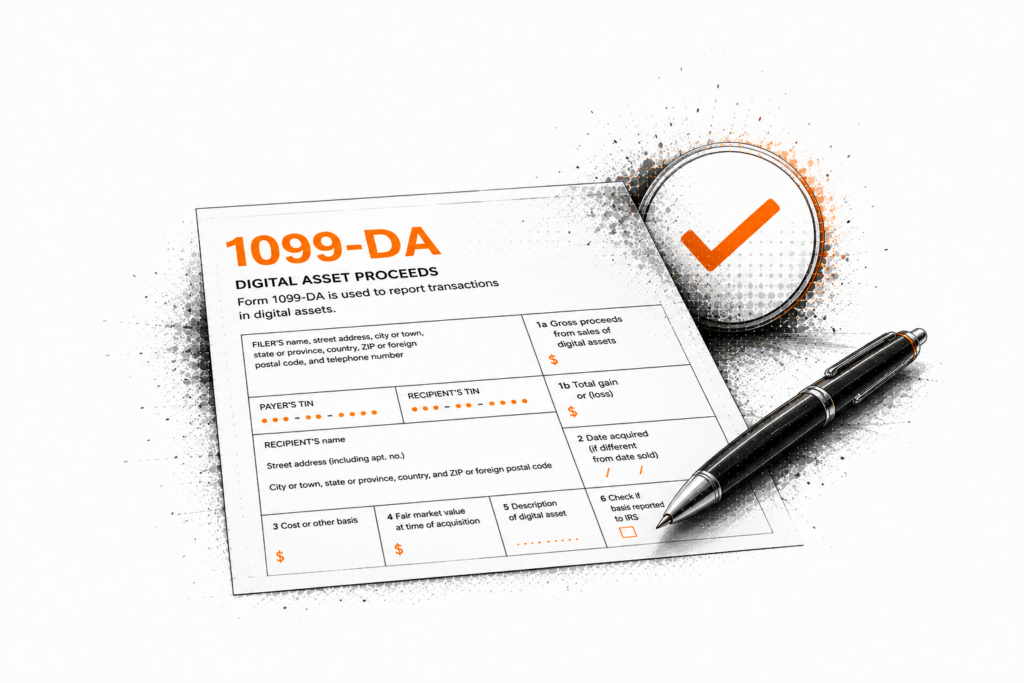

What Is Form 1099-DA?

Form 1099-DA is an IRS information-reporting form designed to capture certain digital asset transactions conducted through U.S.-based brokers. It is intended to standardize how proceeds from activities such as selling, exchanging, or using digital assets are reported.

The form applies specifically to broker-reported transactions, meaning it is generated by platforms or intermediaries that facilitate digital asset activity and have a reporting obligation. Its purpose is to support greater transparency and consistency in how digital asset transactions are documented and communicated to both taxpayers and the IRS.

What Transactions Are Reported on Form 1099-DA?

Sales and Exchanges of Digital Assets

Form 1099-DA may include transactions involving the sale or exchange of digital assets conducted through a broker. This can include selling cryptocurrency for cash or swapping one digital asset for another, where a reporting intermediary is involved.

Converting Digital Assets to Cash or Property

Transactions where digital assets are redeemed or converted into fiat currency or other forms of property may also be reported. These types of liquidation events can trigger reporting when facilitated through a U.S.-based broker.

Payments Using Digital Assets

In certain cases, using digital assets to pay for goods or services may be included if a broker has a role in the transaction. This can apply when digital assets are used as a form of payment and the transaction is processed through a reporting platform.

Who May Receive Form 1099-DA

Form 1099-DA may be issued to individuals who engage in certain digital asset transactions through U.S.-based brokers with reporting obligations. This can include activities such as selling cryptocurrency, exchanging one digital asset for another, or using digital assets for payments when those transactions are facilitated by a reporting platform.

In contrast, there are situations where this form may not be issued. For example, simply holding digital assets, transferring assets between personal wallets, receiving digital assets as a gift, or using platforms that are not classified as U.S.-based brokers may not trigger Form 1099-DA reporting. However, even in cases where a form is not issued, individuals may still have reporting obligations depending on the nature of their activity.

Situations Where Form 1099-DA May Not Apply

There are certain types of digital asset activity where Form 1099-DA may not be issued, particularly when no broker-facilitated transaction is involved. These situations can include:

- Buying and holding digital assets without selling or exchanging

- Transferring assets between personal wallets you control

- Receiving cryptocurrency as a gift

- Certain transactions conducted outside of U.S.-based broker platforms

While these activities may not trigger a Form 1099-DA, they may still have tax or reporting considerations depending on individual circumstances.

What Is Cost Basis in Digital Asset Reporting?

Cost basis generally refers to the original value of a digital asset at the time it was acquired, including the purchase price and, in some cases, associated transaction fees. It is one of the key components used to determine whether a transaction results in a gain or a loss.

For example:

- You purchase a digital asset for $1,000

- You later sell it for $1,200

- The difference of $200 represents a gain

In this scenario, the gain, not the total sale amount, is typically used when calculating potential tax implications. Maintaining accurate records of transactions, including purchase prices and dates, can help support more precise reporting.

It is also important to note that in early phases of Form 1099-DA implementation, some reported data may not include complete cost basis information, depending on how reporting requirements are applied.

How Form 1099-DA Relates to Crypto IRAs

In general, Form 1099-DA is not expected to apply to transactions that occur entirely within certain retirement account structures. This includes self-directed IRAs that are designed to hold digital assets under existing retirement account rules.

Within these structures, transactions such as buying, selling, or exchanging digital assets are typically not subject to taxation. Because of this framework, broker-level reporting requirements like Form 1099-DA may not apply to activity that remains inside the IRA.

This difference reflects how retirement accounts are structured under U.S. tax rules. While broker-reported transactions in taxable accounts may generate reporting forms such as 1099-DA, activity within an IRA is generally governed by a separate reporting system and may instead be reflected through other forms associated with retirement accounts.

When You May Still Receive Form 1099-DA

Even if digital assets are held within a retirement account, Form 1099-DA may still apply to activity that occurs outside of that structure.

You may receive Form 1099-DA if you engage in broker-facilitated digital asset transactions in taxable accounts. This can include selling cryptocurrency, exchanging one asset for another, or using digital assets for payments through a reporting platform.

Form 1099-DA may also be issued when digital assets are redeemed for cash or other property outside of a retirement account. In these cases, the transactions fall under standard broker reporting requirements rather than retirement account reporting frameworks.

As a result, individuals who hold digital assets both inside and outside of retirement accounts may encounter different reporting forms depending on where and how the transactions take place.

Why the IRS Introduced Form 1099-DA

Form 1099-DA is part of a broader effort to standardize how digital asset transactions are reported within the U.S. tax system. As digital assets have become more widely used, reporting frameworks have evolved to provide more consistent and structured information across market participants.

One of the primary goals of Form 1099-DA is to increase transparency by requiring certain intermediaries, such as U.S.-based brokers, to report transaction data in a more uniform way. This approach is intended to improve visibility into digital asset activity while helping align reporting practices with existing financial systems.

The introduction of Form 1099-DA also reflects a move toward integrating digital asset reporting with traditional tax reporting models. Similar to other 1099 forms used for stocks and securities, it establishes a standardized format for reporting proceeds from broker-facilitated transactions involving digital assets.

Understanding Digital Asset Reporting Requirements

As digital asset reporting frameworks continue to evolve, understanding how forms like 1099-DA function can help provide clarity around broker-reported transactions. These reporting standards are part of a broader shift toward more structured and consistent oversight of digital asset activity.

Staying informed about how different transactions are reported, and how they may be treated across taxable accounts and retirement structures, can help individuals better interpret the information they receive from reporting platforms and maintain accurate records over time.

Frequently Asked Questions About Form 1099-DA

What is Form 1099-DA used for?

Form 1099-DA is used to report certain digital asset transactions facilitated by U.S.-based brokers. It is intended to provide information about proceeds from activities such as selling, exchanging, or using digital assets.

Who issues Form 1099-DA?

Form 1099-DA is issued by U.S.-based brokers or platforms that facilitate digital asset transactions and have reporting obligations under IRS guidelines.

Do I need to report crypto if I don’t receive a 1099-DA?

In general, tax reporting obligations may still apply even if a Form 1099-DA is not issued. Reporting requirements depend on the nature of the transaction, not solely on whether a form is received.

Does holding crypto trigger a 1099-DA?

Holding digital assets without selling, exchanging, or using them typically does not trigger Form 1099-DA. The form is generally associated with transaction activity rather than passive holding.

How is Form 1099-DA different from Form 1099-B?

Form 1099-DA is designed specifically for digital asset transactions, while Form 1099-B is traditionally used for reporting proceeds from broker transactions involving securities such as stocks and bonds.

Does every crypto transaction get reported on Form 1099-DA?

Not all transactions are reported on Form 1099-DA. Reporting generally applies to certain broker-facilitated transactions, and the scope may depend on regulatory requirements and the type of activity involved.

3,500+ 5-Star Reviews

3,500+ 5-Star Reviews